Table of Contents

Jan 4 – Welcome to the home for real-time coverage of markets brought to you by Reuters reporters. You can share your thoughts with us at [email protected]

OMICRON’S GAUGES OF FEAR AND GREED (1218 GMT)

Europe’s Travel & Leisure index shows no sign of slowing down and has even gradually accelerated during morning trading to a 3.5% rise, which would be its fourth best performance in the last 12 months.

Register now for FREE unlimited access to Reuters.com

Register

That obviously tells a lot about how investors currently feel about Omicron and the scale of the threat it poses to the economy moving forward.

“The gains for oil firms, airlines and hotel, pub and restaurant operators reflect diminished investor concern about the Omicron variant of Covid-19 amid hopes it is milder, if more transmissible,” summed up AJ Bell investment director Russ Mould.

Hargreaves Lansdown analyst Susannah Streeter also took the view there’s potentially plenty of pent-up demand.

“With so many people in the short-term being forced to isolate at home, it’s likely many people will be spending the next few weeks browsing travel blogs for inspiration, given there is so much desperation for a holiday,” she added, noting that other stocks like cinema operators were rising too.

But there’s another indicator that investors are looking at to gauge the fear and greed waves triggered by the new variant and that’s the yen, which fell to a five year low against the dollar.

At 116.14 per dollar, a level not seen since January 2017, it seems the safe-haven currency is good market gauge of the lack of fear markets currently feel about Omicron.

The rally in bond yields which comes with risk-on moves is indeed clearly felt on the Japanese currency.

“Dollar/yen hit a new 5-year high in the aftermath as traders cut their exposure to haven assets and rate differentials widened against the yen, courtesy of the Bank of Japan’s strategy that keeps a ceiling on Japanese yields”, wrote XM analyst Marios Hadjikyriacos.

(Julien Ponthus and Elizabeth Howcroft)

*****

NEW DAY, NEW MILESTONES (0950 GMT)

Because the STOXX 600 reached a historic peak yesterday, there’s little surprise that a second day of gains across Europe brings in new milestones.

Anyhow, the pan-European index reached a new record of 493.64 points:

Same goes for France’s CAC 40 which is also on uncharted highs for another session at 7288 points:

There are other sectors which are also reaching new records such as industrials at 811 points, Personal & Household Goods at 1,118 points, Construction & Materials at 652 points and Food & Beverages at 883 points.

But while continental stocks continue to march higher, it’s worth noting that London’s FTSE 100, which is outperforming today with a 1.2% rise, is still over 5% away from its May 2018 record:

(Julien Ponthus)

*****

OF BLACK AND GREY SWANS (0909 GMT)

Struggling stocks, a very hawkish Federal Reserve and rallying gold prices are some of the surprises that markets would do well to focus on in 2022, according to Byron Wien, vice chairman and Joe Zidle, chief investment strategist at the Private Wealth Solutions group at private equity giant Blackstone.

Defining a “surprise” as an event that the average investor would only assign a one out of three chances of occurring but which Blackstone’s Wein believes is “probable,” or having a better than 50% likelihood of happening, he lists 10 surprises markets would do well to focus on this year.

Some of the other notable ones include, inflation pressures becoming more entrenched, nuclear alternatives for power generation enters the arena and ESG initiatives become more widespread with government agencies enforcing new regulatory standards on the subject. For a full list, see: https://www.blackstone.com/news/press/byron-wien-and-joe-zidle-announce-the-ten-surprises-of-2022/

(Saikat Chatterjee)

*****

LONDON TAKES OFF WITH TRAVEL AND LEISURE (0832 GMT)

Britain’s travel and leisure stocks are shining this morning and are the uncontested leaders of the pan-European STOXX 600.

BA owner IAG, Ryanair, Wizz Air and TUI are up roughly between 6% and 8.5% and pulling the sector up to a 2.7% rise in early trading.

There’s definitely some optimism in the air that Omicron will not pose a long term threat to the economic recovery.

London, which was closed yesterday for a bank holiday was catching up with the overnight rally and the FTSE 100 up 1.1%, at roughly twice the speed of the STOXX 600′ 0.5% gain.

The optimism for the new year is well spread across sectors. Energy, miners, banks, automotives and retail were all rising over 1%.

Here’s how the Travel and Leisure sector is doing this morning:

(Julien Ponthus with Tommy Lund)

*****

PARTY LIKE IT’S 2022 (0756 GMT)

While many New Year Eve celebrations across the world were scaled down or cancelled due to the surge of the Omicron coronavirus variant, financial markets had a party of their own on the first day of trading of 2022.

A new record high was set on Monday for the pan-European STOXX 600 and on Wall Street, the S&P 500 (.SPX) and the Dow Jones (.DJI) closed at historic peaks.

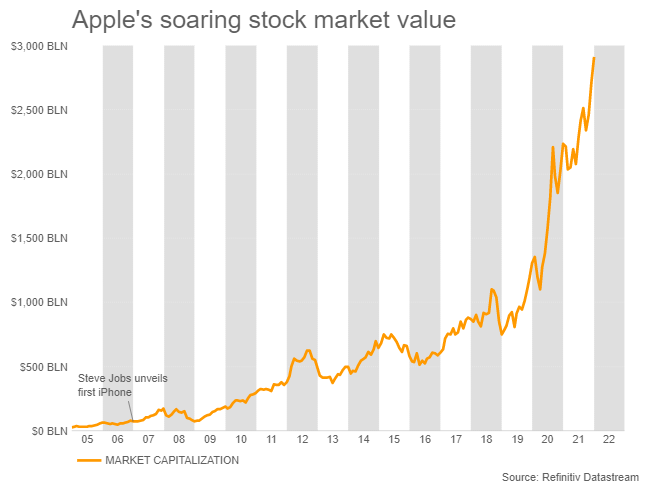

The euphoria surrounding stocks was best captured by Apple (AAPL.O) hitting $3 trillion of market capitalization, which is well above the combined value, for instance, of all the blue chips listed on London’s FTSE 100 (.FTSE).

U.S. Treasury yields also surged as the optimism for the economic recovery had some investors bracing for earlier-than-expected interest rate hikes by the Federal Reserve.

Yields on U.S. 2-year notes, sensitive to rate hike expectations, soared to their highest since March 2020, when the pandemic triggered market turmoil. read more

Other asset classes also enjoyed the risk-on mood such as oil, which rose on hopes of further demand despite OPEC+ looking set to agree to another output increase. read more

Simply put, there’s a bullish consensus that the unprecedented wave of COVID-19 infections won’t derail the global recovery and that vaccines will prevent the need for stringent lockdowns.

Of course, this narrative can be seen as a leap of faith on the supposed milder nature of Omicron and that other factors at play, such as inflation, a policy mistake or politics don’t suddenly rock the boat.

In the meantime, Asian stocks were upbeat on Tuesday and European and U.S. stock futures point to another session of gains.

China Evergrande’s shares jumped as much as 10% in resumed trade after the developer said a government order to demolish 39 buildings on the resort island of Hainan would not affect the rest of its project there. read more

And data showing China’s factory activity growing at its fastest pace in six months in December and German sales unexpectedly rising in November could fuel further optimism.

Key developments that should provide more direction to markets on Tuesday:

–German retail sales rebound in November read more

–Switzerland, France CPI data

–UK mortgage data

–Oil prices edge higher ahead of OPEC+ output policy meeting read more

(Julien Ponthus)

*****

LONDON READY TO CATCH UP (0747 GMT)

The London stock market was off on a bank holiday yesterday and therefore missed the New Year party across global markets.

It seems there’s been quite a lot of Fomo building up and that investors are ready to play catch-up.

Futures for the FTSE 100 are currently up over 1%.

Other European bourses are nonetheless expected to go for a second straight session of gains but with rises limited to about 0.5%.

Same trend for U.S. futures which currently point out to another day or record highs on Wall Street.

(Julien Ponthus)

*****

Register now for FREE unlimited access to Reuters.com

Register

Our Standards: The Thomson Reuters Trust Principles.

More Stories

Traveling to Komodo Island: A Simple Guide for an Amazing Adventure

The Ultimate Adventure Guide on Labuan Bajo

6 Paris Travel Attractions Everyone Loves